How Do You Refinance A Loan

/what-is-refinancing-315633-final-5c94f0874cedfd0001f16988.png)

Refinancing What Is It

How To Refinance Your Personal Loan

10 Things To Consider Before Refinancing Your Home Loan Icompareloan Resources I Compare You Save

Refinancing Housing Loan 8 Things To Find Out

Can Refinancing Your Home Loan Actually Help You Save Money

Refinance Home Loan And Cash Out Fully Paid Up Property Icompareloan Resources I Compare You Save

Check your credit scores regularly to ensure you don t get blindsided by negative or erroneous information and avoid taking out new credit before and during the refinance process if possible.

How do you refinance a loan. If you have high interest debt such as credit cards it may make sense to use a cash out refinance to pay off this debt do the math to make sure the all in costs including the closing costs for the cash out refi work out because the interest you pay for your credit card likely far exceeds the interest on your new mortgage loan. There are many reasons why homeowners refinance. This might occur if you do a cash out refinance where you take cash for the difference between the refinanced loan and what you owe on the original loan or when you roll your closing costs into your new loan rather than pay them upfront. As a result you pay less interest over the life of the loan.

You could in fact take on more debt when refinancing. Since refinancing can cost between 2 and 5 of a loan s. So before you shop for quotes determine the exact amount of money required. When you refinance from a 30 year mortgage into a 15 year loan you pay off the loan in half the time.

You won t reduce or eliminate your original loan balance. Refinancing costs money to the tune of several thousand dollars. The first thing you must do when considering refinancing is to consider exactly how you will repay the loan. You may be able to refinance a conventional loan with as little as 5 percent equity but you ll get better rates and fewer fees if you have more than 20 percent equity.

When you refinance a loan you re essentially paying off the existing loan with a new one that has different terms. You ll pay application and origination fees a fee to have your home reappraised and in some cases mortgage points that reduce your new interest rate. If the home equity line of credit is to be used for home renovations in order to increase the value of the house you may consider this increased revenue upon the sale of the house to be the way in which you will repay the loan. Refinancing a mortgage means paying off an existing loan and replacing it with a new one.

While it may be possible to refinance with a higher ltv ratio you may have to pay private mortgage insurance pmi expenses if you do so which can reduce the value of the refinancing. As you consider and apply for a refinance loan it s important to know where you stand with your credit.

How To Refinance Your Home Loan In Singapore Save Money On Your Mortgage Moneysmart Sg

How Can You Refinance Your Home Loan To Save On Your Mortgage Bettertradeoff Financial Life Planning Singapore

4 Reasons Why Refinancing Using The Cheapest Home Loan Isn T Always The Best Move 99 Co

How To Refinance Your Home Loan In Singapore Save Money On Your Mortgage Moneysmart Sg

Should I Refinance My Housing Loan 10 Things To Consider Invest News Top Stories The Straits Times

How Can You Refinance Your Home Loan To Save On Your Mortgage Bettertradeoff Financial Life Planning Singapore

Reprice Vs Refinance Home Loans In Singapore What S The Difference Propertyguru Singapore

Rate And Term Refinance Definition

4 Must Knows Before Refinancing Into A Low Interest Sibor Home Loan 99 Co

Why Should I Refinance My Mortgage Or Home Loan Mortgage Supermart

Infographic Ultimate Guides Home Loan Refinancing In Malaysia Wma Property

/pros-and-cons-of-refinancing-a-car-loan-1a117a027ee14bd583fd1abdef935b9d.gif)

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gctudb6s6jk 0 Uznplp Vnly7lja Nbfkbcmw Usqp Cau

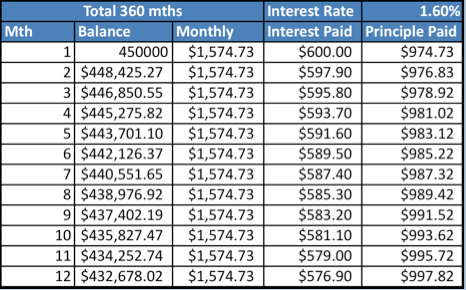

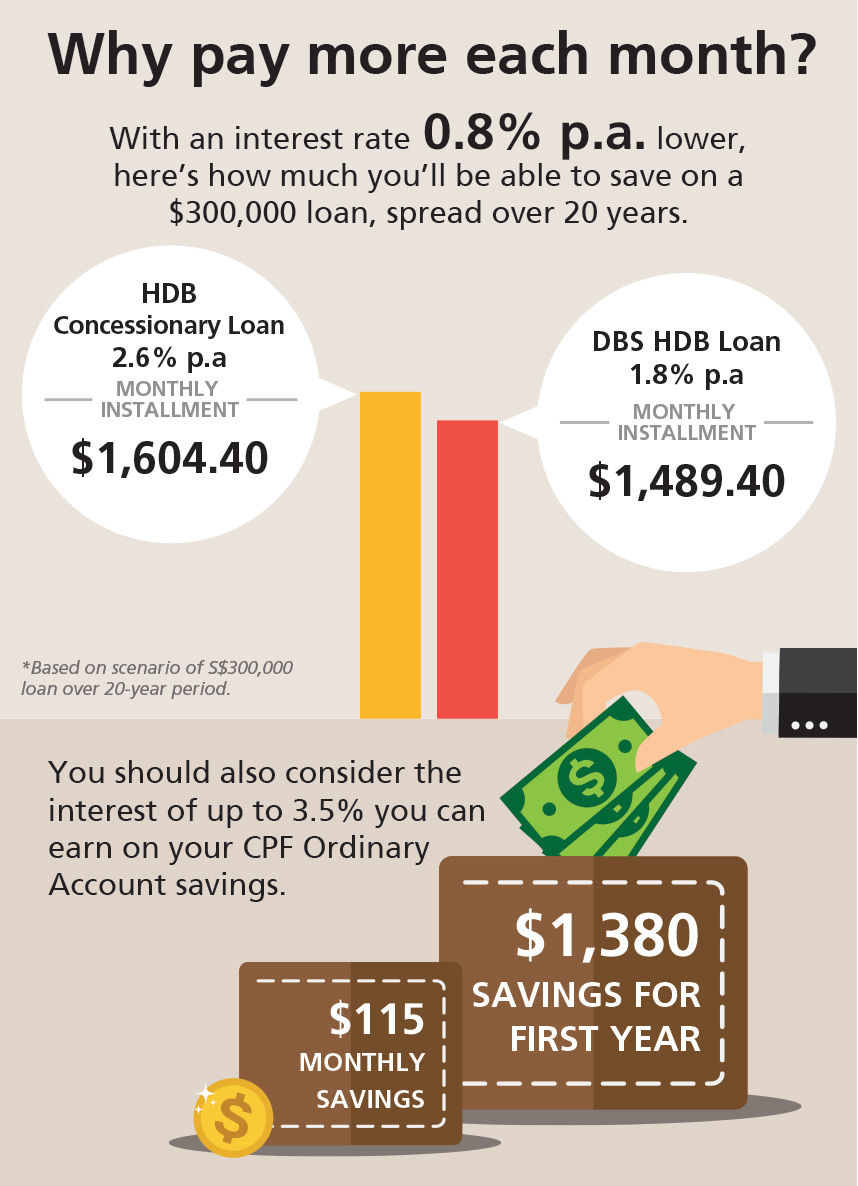

Refinancing Your Housing Loan Hdb Loan Vs Bank Loan Dbs Singapore