Factoring With Recourse Accounting

Factoring Accounts Receivable Definition Explanation Journal Entries And Example Accounting For Management

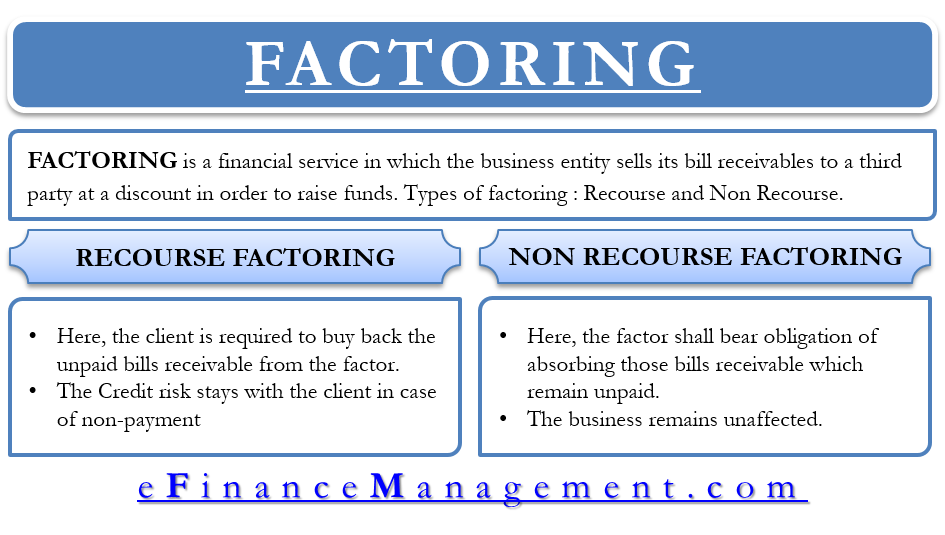

Recouse Factoring And Non Recourse Factoring Definition And Difference

Accounts Receivable Factoring Learn How Factoring Works

Factoring Accounts Receivable Definition Explanation Journal Entries And Example Accounting For Management

Factoring Of Accounts Receivable Accounting Definition Journal Entries Example With Recourse Without Recourse

Accounts Receivable Factoring Learn How Factoring Works

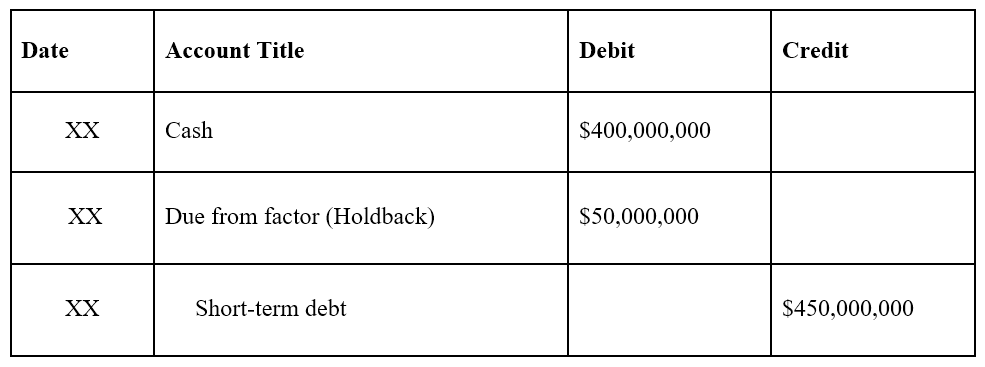

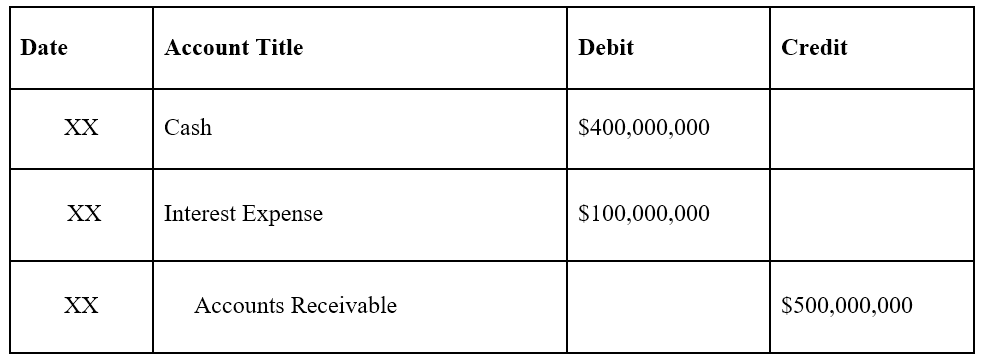

100 million is considered interest expense.

Factoring with recourse accounting. Home accounting tutorials assets in accounting recourse in factoring recourse in factoring recourse is a type of factoring which happens when an entity has to sell the invoices to the client factor with a condition that the entity will purchase back any invoices that remains uncollected this means that in recourse the factor client is not taking any risk of the uncollected invoices. Non recourse does not necessarily protect your company from all risk though. In a factoring with recourse transaction the seller guarantees the collection of accounts receivable i e if a receivable fails to pay to the factor the seller will pay. A short term quick solution that can bring cash and help the company meet its short term obligations.

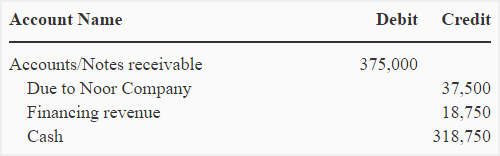

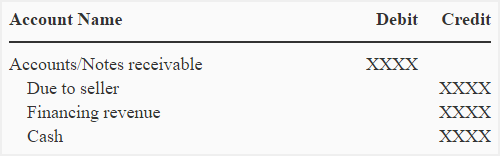

Your business sells accounts receivable with recourse to the factoring company on january 1st. Non recourse factoring means the factoring company assumes most of the risk of non payment by your customers. The journal entry would be as follows. An example of recourse factoring and non recourse factoring is shown below.

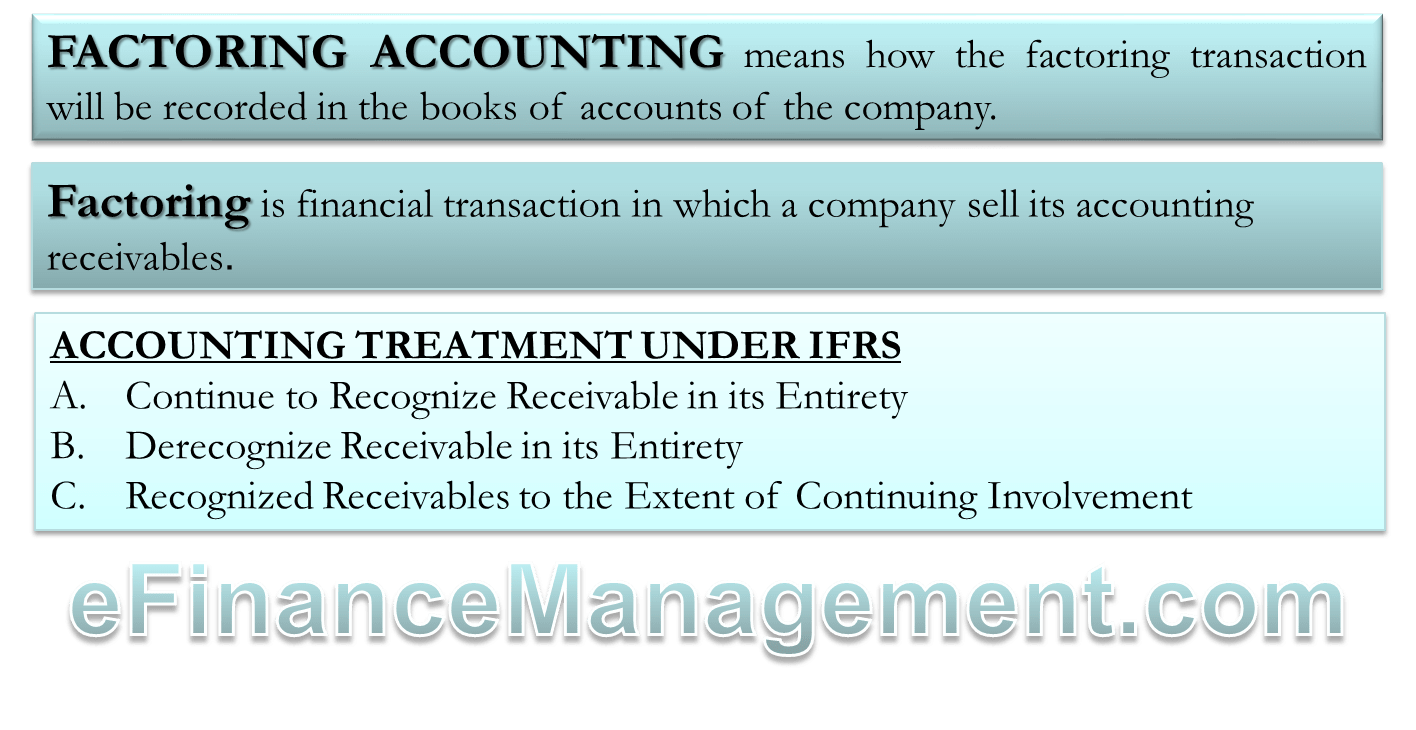

Examples of accounts receivable factoring. Accounting standards ifrs and gaap distinguish two different cases factoring with recourse and factoring without recourse. Company a transfers 500 million of receivables without recourse for proceeds of 400 million.

Factoring Receivables Double Entry Bookkeeping

Factoring Accounts Receivable Definition Explanation Journal Entries And Example Accounting For Management

Recourse In Factoring Meaning Overview Example With Journal Entries

Accounts Receivable Factoring Learn How Factoring Works

Accounts Receivable Factoring With Recourse Sales Of Accounts Receivable Youtube

Accounts Receivable Factoring Examples How It Works

Recourse Versus Non Recourse Factoring What S The Difference

Factoring Receivables

Factoring Accounting Meaning Accounting Treatment Journal Entries

How To Record Invoice Factoring Transactions Accounting

Factoring With Recourse Annualreporting Info

Accounts Receivable Factoring With Recourse Versus Without Recourse On Sale Youtube

Factoring In Practice Advanced Financial Controlling Tools And Articles